Payments Systems in the US by Carol Coye Benson, Scott Loftesness and Russ Jones was among the most informative books I read on the financial services industry. Below are some key snippets I’d like to retain and share.

Economic Models for Payment Systems

The payments industry is different from other processing industries in terms of the value of money being transferred through the system. Providers who realize revenue related to gross value of the payment transaction (the “amount”) are more likely to have profitable businesses than those who realize revenue simply on a fee-per-transaction basis.

The Network Business (i.e. Mastercard, Visa)

- Handles transaction switching among banks participating in network

- Net settlement among banks, usually on daily basis and include multi-currency settlement

- Creation, updating, maintenance and enforcement of operating rules

- Management of network membership

- Creation and maintenance of brands and brand promotion strategies

- Arbitration of disputes between network participants

Card Network Interchange

Used by card networks, interchange is a transfer of value from one intermediary in a payments transaction to the other intermediary in that transaction. The system/network sets interchange prices, but does not receive the interchange. Interchange creates incentive for one “side” of the transaction to participate, by having the other “side” reimburse some of the costs incurred.

Originally introduced to bring into balance the costs borne by the card issuer and the merchant acquirer to provide the card payment service.

Rests on the concept that one “side” of the transaction, the merchant (and its acquiring bank) benefits from the use of the card (primarily through increased merchant sales) while the other “side”, the card issuer, incurs costs associated with making this use possible.

Interchange is the mechanism the card network established early on to have the value-receiving merchant compensate the cost-incurring issuer for the issuer’s expenses.

These costs include:

- Cost of guarantee: Issuer extends payment guarantee to the merchant. Merchant will be paid even if cardholder subsequently fails to pay the card issuer what he or she owes.

- Cost of funds: Merchant receives payment from issuing bank (via card network) before issuing bank is paid by the cardholder

- Operating expenses: Issuing bank has expenses in operating its authorization network, producing statements, handling customer service, etc.

In the US, interchange flows from acquiring bank to issuing bank on purchase transactions. It is therefore an expense to the acquiring bank and a revenue to the card issuing bank.

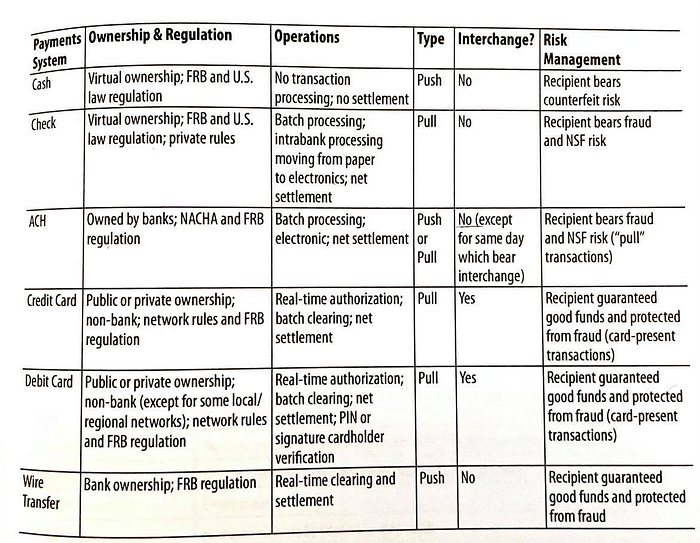

ACH and wire transfers do not have interchange. However, the ACH system recently approved a new processing model, “same day ACH,” which has an “interchange” component.

Risk Management

3 major forms of risk

- Credit Risk: credit card issuer bears credit risk since cardholder may simply fail to repay his or her loan balance.

- Fraud risk: different types of payments fraud risk depending on the system (theft, fraud)

- Liquidity risk: The risk that a party cannot fulfill its financial obligations to another party. A bank receiving money from another bank in the system need not worry about liquidity of sending bank. But the network does have to worry, since if a network member fails during the day while in a net debit position, the network must pay obligation of that member to other members.

Card Acquiring

What is an Acquirer?

- From the merchant’s perspective, the “acquirer” is the entity that sold the merchant a merchant account, with whom the merchant deals on a day to day basis.

- From a card network’s perspective, it’s the bank that belongs to the card network and has contractual ability to the network for actions of its clients in handling payments within that network.

- From the industry perspective, it is the bank or non-bank processor bundling most of the functions in the value chain.

Economics of Acquiring

As an example: If you are making a purchase at your favorite coffee shop, the acquirer is the coffee shop (merchant)’s bank.

Acquiring revenue is largely based upon merchant discount fee: the price charged by the acquirer to the merchant. Normally expressed as fixed fee + a percentage of the value of the transaction.

Card interchange fee (charged by issuer to the acquirer) are such an important component of acquiring expense, that the acquirer often prices services to the merchant as an “interchange plus” basis.

A merchant discount fee, therefore, may have a price of “interchange plus assessments” plus “x cents per transaction plus y% of the transaction value.”

Expenses of an acquirer:

- interchange fees

- card network assessments

- merchant acquisition costs

- systems development, maintenance, compliance

- processing costs

- merchant servicing costs

- credit losses

- fraud losses

Why the credit and fraud losses? Because a fraudulent merchant will result in cardholder disputes and chargebacks on those transactions back to the merchant. If merchant has disappeared, or if its account cannot fund the chargebacks, the acquirer bears the financial responsibility. Because fo this, fraud management of merchant accounts is an important part of the acquirer’s job.

Uses of the ACH System

Large and small enterprises, including corporations, governments, nonprofits use ACH to make payments to and collect payments from consumers

Preauthorized Consumer Transactions

- PPD (prearranged payment and deposit): credit transactions are used for payroll, pension, benefit payments to consumers. This is the system behind your bi-weekly or monthly paycheck deposit.

- PPD Debit transactions: used primarily for recurring bill payments

Business-to-Business Transactions

- CCD (Corporate Credit or Debit) Credit transactions are used for supplier payments, in lieu of checks. Debit transactions may also be used for supplier payments when corporate customer gives a trusted supplier the ability to debit its account

- CCD Debit transactions are frequently used for intracompany funds concentration. Corporation with bank accounts in multiple states may use ACH to pull funds into single account for investments

- CTX (Corporate Trade Exchange) Credit transactions are similar to those via CCD Credit but designed to carry addenda records with each financial transaction.

Card Risk Management

Credit Risk

- Credit card issuer takes on credit risk when extending line of credit to new cardholder. Issuers control this risk through a credit approval process at the time of account opening, and via periodic reviews of the cardholder’s account and behavior.

- Charge card issuers also take credit risk, but for a shorter time period, as cardholders are expected to repay account balances at the end of each billing period.

- Debit card issuers take no credit risk unless they authorize a transaction against insufficient funds, thereby approving an overdraft loan to the consumer. In doing so, they have credit risk exposure similar to that of the charge card issuer.

Fraud Risk

One of the most important functions played by card networks is the accumulation of fraud data from issuers (issuers must report fraud when discovered), and the analysis of that data.

For both credit and debit cards, there is a major difference in rules between card-present and card-not-present environments.

- Card-present acceptance environments: fraud liability is allocated to the card issuer

- Card-not-present: Liability is allocated to the card acquirer (ultimately borne by card-not-present merchant)

If cardholder claims “I didn’t do it (make the purchase)” and the transaction occurred at physical store, then when the cardholder’s account is credited, the card issuer bears the loss. Merchant keeps the sale.

If transaction occurs at online retailer, the card issuer can charge back the transaction to the acquirer — which then debits the merchant’s account.

Types of Card Fraud and Fraud Control Mechanisms

- Lost and stolen fraud

- Counterfeit fraud: card’s magnetic stripe data has been duplicated on new piece of plastic and issued by fraudster. Popular fraud was easy to pull off in early days of credit cards when counterfeit card could be created from just the data visible on the card (name, expiration date, account number). In today’s market, the card system is moving to chip cards, which should make counterfeit fraud much more difficult.

- Card not received fraud: newly issued card stolen en route to legitimate cardholder

- Identity theft

- Identity creation

- Unauthorized use: legitimate card account used by unauthorized individual in card-not-present environment

- “Bust out” fraud: legitimate card account used by individual with no intent to pay off the balance. Controlled by same tools used to monitor credit risk exposures.

- PIN debit fraud: fraud in card-present environments is limited. What occurs is theft of both pin and physical card, i.e. fake ATM front accepts and reads magnetic stripe of debit card, while hidden camera records pin entry.

A risk-adjusted profit margin for an issuer is:

Profit = revenue from interchange - (fraud losses + credit losses)

Cash Volumes

- 60% of cash produced by US is held overseas

- 96% of all purchases in India are made by cash. Over 90% of residents are unbanked

Cross-border Payments

- Payments systems, by definition, operate on an in-country basis: only banks that are chartered or licensed to operate in a country may join a payments system in that country. Due to this, transferring money between countries often requires two separate transactions: one in the sending country and one in the receiving country. True even if transaction is denominated in the same currency in both systems.

- Each transaction must go through two payments systems, in two different countries. Intermediary banks settle their positions through correspondent accounts with each other, or with a third bank.

How Banks Make Money

- Lending money

- Holding money (in deposit accounts of investment accounts)

- Moving money — moving money means payments.

All three are profitable, but relative profits are highest for lending. Deposit taking is profitable on its own, but is particularly valued as source of funds for more profitable lending business.